Energise your drinks sales this summer

Now worth more than £10bn, the total UK soft drinks market maintains its spot as a top-three category in convenience. Across summer 2023, soft drinks in convenience saw a 21% increase versus the February to May period.

While consumer habits have changed, with the pandemic and the cost-of-living crisis all having an impact on what purchases they make, retailers have an opportunity to tempt their tastebuds and increase sales in store.

Remaining a dominant force in the market, a high proportion of Northern Ireland consumers purchase each year – in the 52 weeks ending 18th February 2024 99.5% of NI households purchased the category versus 99.2% last year^.

Its market worth = £201,198,000 +14.3% year-on-year with shoppers spending an additional £25.2 million versus last year.

Across the UK soft drinks market, at-home revenue amounts to £22.20bn in 2024, with the market expected to grow annually by -1.18%*.

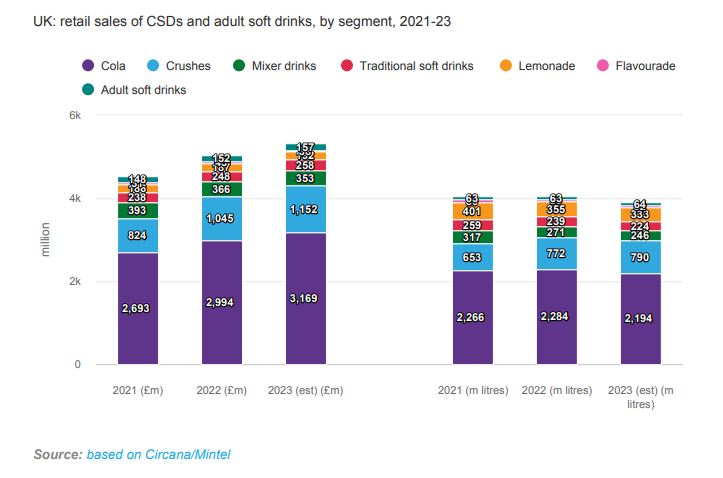

Carbonated soft drinks accounted for 39.9% of the category share in 2022**, while across the calorie sector, demand is significantly increasing for low/no calorie soft drinks, claiming a 69.8% share in 2022**.

The volume sales of low/no calorie carbonated drinks grew by 11.9% during 2022**, while there was a 24.3% growth in volume sales in sports drinks across the same year**.

According to the 2023 British Soft Drinks Association report, volume sales of sports and energy drinks grew by 24.3% in 2022, with continued growth expected across 2023 and beyond. In 2022, the channel split was 94.7% off premise with 5.3% on premise.

In its five-year outlook for carbonated soft drinks, Mintel forecasts that health and sustainability will be key driving factors for consumers as they choose their CSDs.

The market was hit in 2023 by the income squeeze, rising prices in the category and poor summer weather. Price rises fuelled value growth, tempered by trading down.

The income squeeze took its toll on CSDs on-premise sales in 2023. While some occasions moved to retail, sales through this channel also stagnated amid the income squeeze and less clement summer weather.

Cola leads CSD retail sales by a long distance, while the leading players’ ongoing marketing and NPD drive engagement. Crushes were the star performer in 2023, bucking the volume decline in CSDs in retail, with high-profile flavoured launches a key driver.

With household budgets expected to remain under pressure in 2024, CSDs volumes will see little improvement, while value growth will slow as inflation decelerates, according to Mintel.

In their overview of how they expect the carbonated soft drinks category to perform over the coming five years, Mintel draws on its expertise in the market, market forecast and understanding of the key trends that are driving consumer behaviour.

It does predict real-term growth in 2025-2026, as household incomes regain momentum so too do they expect CSDs volumes to also regain momentum.

This will also facilitate trading up, including to on-premise, fuelling faster value than volume growth. The planned introduction of DRS in 2025 could bring disruption, but the industry is in a position to minimise this.

Looking ahead to the future (2027-2028), Mintel forecasts that health and sustainability will be more front of mind issues for consumers, firstly because of their improved finances and then this necessitates continued progress in both areas from brands.

The decline in 20-34s will pose headwinds, but the considerable appeal of new flavours holds potential for CSDs to continue to drive engagement, Mintel adds.

As observed in the British Soft Drinks Association’s 2023 annual report, 2022 was a healthy year for soft drinks, with volume sales up by nearly 8% on 2021 and low/no calorie drinks accounting for seven out of every 10 purchases made in the calendar year.

Ben Parker, GB Retail Commercial Director at Britvic said consumers have been feeling the pinch from rising living costs and inflation, with more shoppers being mindful of what they spend.

“In a bid to make their money stretch further, these pressured shoppers are expected to move toward smaller transactions and smaller pack sizes,” said Ben.

“At the same time, we’re also seeing a ‘lipstick effect’ where shoppers are switching from expensive purchases to treating themselves with smaller treats and indulgences.

“We have seen the trend for healthier products continue to increase among consumers and with the high in fat, salt and sugar (HFSS) regulations now in place, reduced sugar options when it comes to soft drinks will only continue to grow in importance,” he added.

“As a category, soft drinks was well prepared ahead of the legislation, following the introduction of the Soft Drinks Industry Levy which came into effect in 2018. Therefore, to date, soft drinks has been in an ideal position to help retailers with any shortfall from other non-HFSS categories,” said Ben.

“Flavour innovation is crucial in keeping shoppers excited by soft drinks and at a time when the cost of living is rising, it’s important to offer new products from well-known brands to help maintain basket spend.”

Looking ahead in 2024, Mintel forecasts a continued growth for the energy drinks market, but urge brands not to rely on past successes, stating innovation and evolving is key as the competitive landscape constantly shifts consumer demand.

“Interestingly, as the user base of energy drinks grows and diversifies, brands have begun to distance themselves from an overtly masculine image, which could open the door to even more growth amongst demographics who had previously slept on the energy drinks industry,” say Mintel.

“Over the past few years, consumer demands in the energy drinks industry have shifted. An increased focus on health has resulted in consumers looking for more than a sugary, caffeinated pick-me-up.

“More and more consumers want functional drinks that can help them achieve their health goals, rather than potentially hinder them.”

TO SEE THE FULL ENERGY AND SOFT DRINKS FEATURE IN THE MAY ISSUE OF NEIGHBOURHOOD RETAILER, CLICK HERE

^Kantar

*statista.com

**British Soft Drinks Association 2023 annual report