Northern Irish shoppers show preference for brands despite economic pressures

Grocery inflation is now standing at 8.5% for June – the ninth consecutive month of decline and now sitting at a level last seen in December 2022.

The latest figures from Kantar show that take-home grocery sales grew with shoppers visiting store more often, on average shoppers made nearly three more trips than last year, however the number of packs per trip purchased continues to fall by 0.2%.

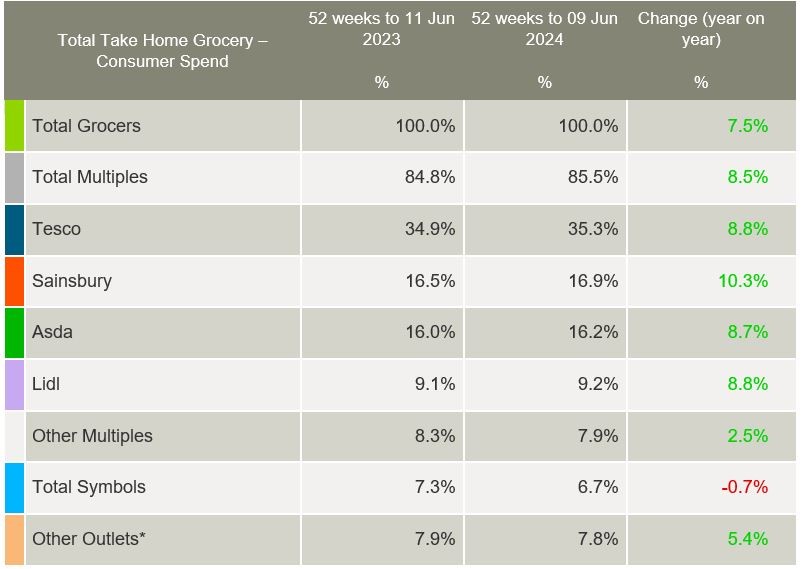

In the year to 9th June 2024, £4.24 billion ran through the tills, up 7.5% year-on-year which equates to an additional £297.7 million versus last year.

Business Development Director at Kantar, Emer Healy said that although inflation levels are falling, they are still high with Northern Irish consumers still facing significant pressures on their household budgets, with the average annual grocery bill is set to rise by £476 from £5600 to £6076 if consumers don’t make changes to what they are buying.

“Own label ranges remain popular as shoppers tighten the purse strings, growing by 8.1% year-on-year with shoppers spending an additional £139 million on these products versus last year,” said Emer.

“Brands grew just ahead of the market at 7.8% year-on-year and hold 54.4% value market share. Our latest Brand Footprint report shows that the average Northern Irish household buying a portfolio of 80 FMCG brands in a year – well above the global average of 66. This shows clearly how brands are still an important choice for Irish consumers.”

‘Own label ranges remain popular as shoppers tighten the purse strings’

Over 22% of sales were made through a promotional offer, a level not seen since October 2020. Bank holiday weekends encouraged shoppers, with them spending an additional £5 million on beer, lager and wine versus last year and £ million more on take-home savouries.

Meanwhile, Tesco maintains its position at the top of the table and is Northern Ireland’s largest grocer with a 35.5% share of the market, with value growth up 8.8%. Tesco welcomed more frequent trips which contributed an additional £86.4 million to their overall performance.

Lidl holds 9.2% market share, with value growth up on 8.8% year-on-year, and they welcomed new shoppers in store which continued an additional £4.4 million to their overall performance.

Sainsbury’s holds 16.9% share, with value growth up 10.3% and also welcomed more frequent trips which contributed an additional £144.4 million to their overall performance; Asda holds 16.2% of the market, with value growth up 8.7% and saw a boost in new shoppers which contributed an additional £16.9 million overall.